Today’s letter is brought to you by Arrived!

Arrived makes it easy to buy shares of rental homes, allowing anyone to earn passive income and benefit from property value appreciation. Simply select from our wide selection of high-quality rental homes and invest anywhere between $100 and $20,000 in each property.

Arrived takes care of the management & operations, so you can sit back and build wealth. Arrived is backed by world class investors including Jeff Bezos & Marc Benioff.

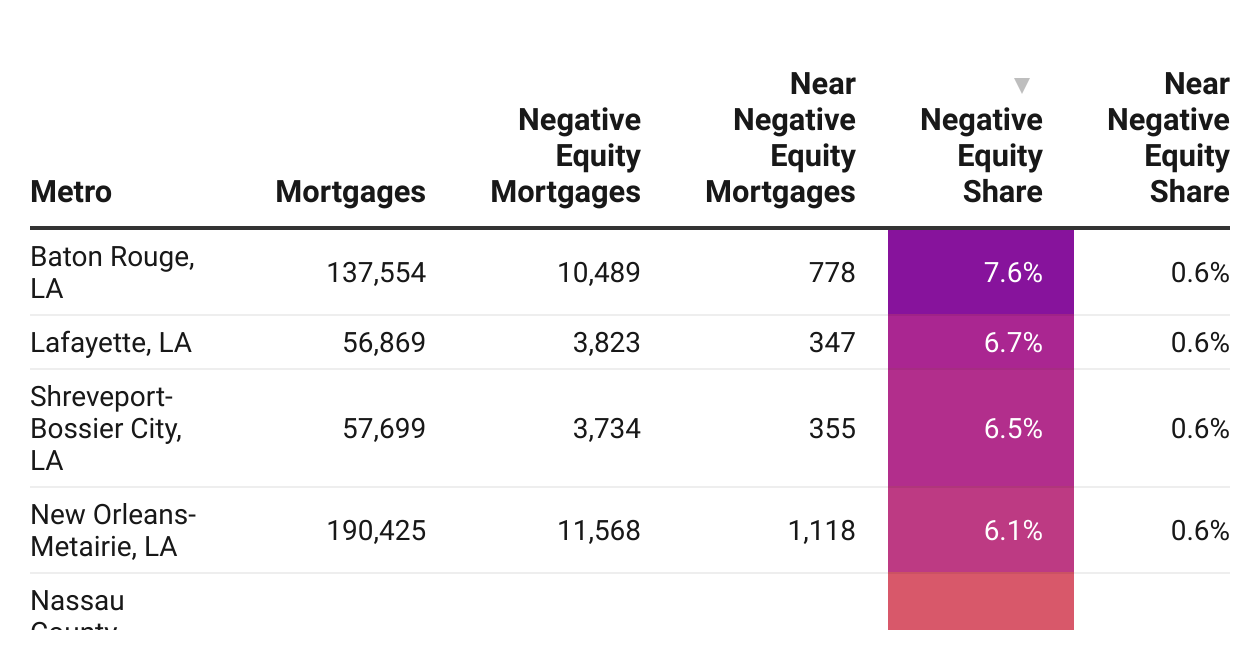

Despite the fact that housing affordability has deteriorated to levels not seen since the '80s, only a fraction of U.S. homeowners have negative equity, meaning they owe more on their house than it’s worth. That’s according to CoreLogic’s Q3 2023 report published this week.

CoreLogic's latest data reveals that across the nation, negative equity affects just a small percentage of mortgage borrowers, with Louisiana leading at 6.1%, followed by Iowa (4.92%), Oklahoma (4.13%), North Dakota (3.71%), and Kentucky (3.42%).

In contrast, states like California (0.63%), Nevada (0.73%), Arizona (0.82%), Florida (1.04%), and Massachusetts (1.12%) boast the smallest percentages of homeowners with negative equity.

The reason few borrowers are underwater? U.S. home prices, as measured by the Case-Shiller National Home Price Index, are up +45.1% since March 2020—including a +1.3% uptick since the average 30-year fixed mortgage rate crossed over 6.0% in June 2022.

Click here for an interactive version of the map below.

Notably, even in markets like New Orleans and Austin, where home prices have declined -11.7% and -18.3%, respectively, since the 2022 peak according to the Zillow Home Value Index, only a modest percentage of local borrowers face negative equity. In New Orleans, 6.1% of local borrowers have negative equity, while that figure is 2.1% in Austin.

Big picture: High levels of homeowner equity suggest that if the U.S. economy does slip into a recession, the current housing cycle is less likely to trigger a foreclosure wave similar to the aftermath of the Great Financial Crisis. Unless home prices materially shift downward, homeowners who do lose their job or see their financial situation head south would be more likely to sell rather than outright foreclose.

Click this link, or the image below, to be taken to a searchable chart displaying negative equity data for 190 metro-area housing markets.

Once you’ve opened the link, you’ll see a search box on the top left side of the chart. Type your market, or your state abbreviation (see “TX” below), in that box.

This weekend, ResiClub PRO members will get access to an interactive map displaying Realtor.com’s “Hotness Score” at a county-level. It’ll also include Realtor.com’s county-level “Demand Score” and “Supply Score.”